If you or a family member have ever been admitted to a hospital or if you sell to hospitals within the USA understanding their charges, costs and payments can be a bit daunting. Hopefully this blog will help to ease the pain and provide a greater level of understanding. In this blog we will cover several terms and topics including:

- Hospital billed charges

- Contractual adjustments taken by insurers

- Allowed amount

- Paid amounts to hospitals (by an insurer or patient)

- Hospital expenses

At the end of this blog it is our hope that you have an appreciation and understanding of why price transparency is both confusing and essential.

Introduction

Hospital billed charges are list prices similar to what medical equipment manufacturers provide as a suggested list price. GPOs, IDNs, hospital systems and individual hospitals typically negotiate from this suggested list price to something below it. In the end, different customers pay different amounts for the same product.

Health insurance organizations (payors) do the same thing. They negotiate private contracts with hospitals for discounts off their billed charges (equivalent to a manufacturers list price), and insurers end up paying different amounts to a hospital for the same procedure. This is called a contractual adjustment.

Are you confused yet?

We know this can be confusing so let’s look at a high-level summary and then provide some detailed context and examples.

The following is a brief summary of the relationship between the terms discussed below:

Hospital Billed Charges – Contractual Adjustments = Allowed Amount

Allowed Amount = Paid Amount by Insurer + Patient Share

Hospital Cost = Hospital Expenses for Providing Care

Let’s look at each of these.

Hospital Billed Charges

Think of a hospital as a hotel. A hotel has a price list and charges you for the room, internet service, food and beverages. A hospital has a price list as well. It is called a “Chargemaster” or Charge Description Master (CDM). It includes medical procedures, lab tests, supplies, medications etc. A hospital charges for every item used by a patient along with its associated charges (billed charges) on every claim submitted to an insurance carrier or patient.

Think of a hospital as a hotel. A hotel has a price list and charges you for the room, internet service, food and beverages. A hospital has a price list as well. It is called a “Chargemaster” or Charge Description Master (CDM). It includes medical procedures, lab tests, supplies, medications etc. A hospital charges for every item used by a patient along with its associated charges (billed charges) on every claim submitted to an insurance carrier or patient.

The billed charges for every item are the same for every payer so there is consistency. In most hospitals, billed charges only cover the hospital’s charges; they do not cover many professional fees. For example, if you are seen in the Emergency Department by a physician that is part of an outsourced service you will receive a separate bill for his/her service. If you need surgery you will also receive an invoice from the surgeon and the anesthesiologist or anesthetist.

Allowed Amounts & Contractual Adjustments

Just because a hospital bills for each item or service doesn’t mean it collects the full amount. In fact, hospital billed charges rarely equal the amount reported in the Chargemaster. In most situations, the amount hospitals actually receive in payment is less than the price appearing on the Chargemaster. Health insurance organizations (payors) negotiate discounts that are referred to as “contractual adjustments.” The size of the discount and how it is determined varies by payer. Let’s look at three (3) examples:

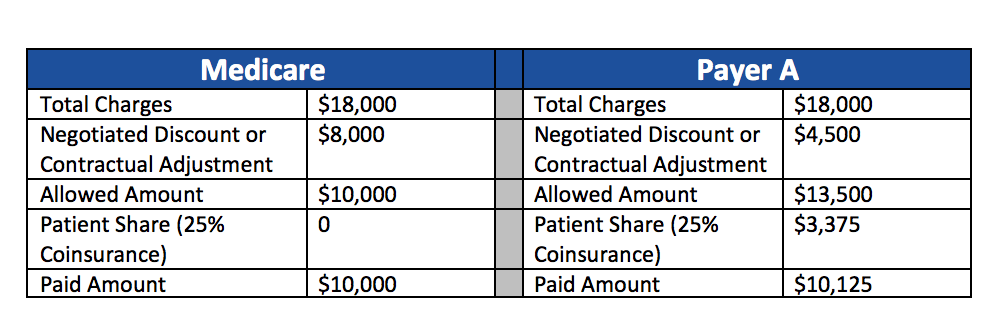

- Medicare is a primary payer for most hospitals. Medicare is a government run federal program that sets the payment rate for each service they pay for and hospitals must agree to these payment levels to participate in the program. This is a condition of participation. A hospital may send an invoice for charges of $18,000 for a specific procedure, but if Medicare has determined the payment level is $10,000 that’s all they will pay. If the hospital submits a claim to Medicare for $18,000, Medicare will only pay $10,000. The remaining $8,000 is considered the contractual adjustment.

- Commercial insurers (example Cigna-Anthem) usually negotiate discounts off the Chargemaster and it is not unusual for each insurer to have a different discount. For example, a hospital and an insurer may enter into a contract in which the insurer agrees to pay 75% of billed charges. In this case, a claim with total charges of $18,000 from the Chargemaster for a specific procedure would result in a contractual allowance of $4,500 and a paid amount to the hospital of $13,500. Another insurer could have a contract at 60% of billed charges for the same claim/procedure of $18,000. In this case the contractual allowance would be $7,200 and the hospital would receive a paid amount of $10,800.

- Since uninsured payments don’t have contractual adjustments they usually bear a much higher price for hospital care than patients with Medicare or a commercial insurer. In some cases hospitals will provide an automatic discount to low-income patients. In other cases these patients may qualify for indigent care. Some states are requiring that the self-pay patient pay no more than the average commercial payor allows and with new IRS regulations regarding financial assistance policies for non-profit organizations, this is part of that policy.

As you can see payer mix and how the hospital negotiates its contract prices makes a huge difference in how much money a hospital receives for its services.

Patient Share

Most health insurance programs require the patient to share in the cost of their healthcare through one of the following methods:

Most health insurance programs require the patient to share in the cost of their healthcare through one of the following methods:

- Copayments (e.g., patient pays $20 per physician visit) or

- Coinsurance (e.g., patient pays 35% of the Emergency Department Amounts) or a

- Deductible (e.g., enrollee pays the first $1,000 of care in a given year).

These cost-sharing arrangements add complexity to the payment process described above.

The actual payment that a hospital receives is known as the allowed amount. This is the maximum reimbursement the health insurance plan will pay the hospital for a service provided to a patient in a hospital, based on the insurer’s contract with the hospital.

Under a cost-sharing arrangement, the allowed amount is then divided between the insurer and the patient. The amount actually paid by the insurer is known as the paid amount. An example will provide clarity.

For example, let’s look at two different payers for the same procedure. In both situations the total charges are $18,000. Medicare only pays $10,000 for the procedure so the contractual adjustment is $8,000 while Payer A pays $13,500 with a contractual adjustment of $4,500.

With Medicare the patient pays zero (this assumes they have a supplemental policy that pays the difference) and the hospital receives $10,000. With Payer A, the hospital receives $10,125 but of that they must collect $3,375 from the patient. As you can imagine this is often difficult for many individuals and it often necessitates a payment plan.

This simple example illustrates why there is confusion with hospital pricing because the pricing is the same but the allowed amount differs based on the negotiated rates with various carriers. To the hospital the price for the procedure is $18,000. To the insurer it is $10,000 for Medicare and for Payer A it is $13,500. For the Medicare patient it is zero and for Payer A it is $3,375.

Hospital Costs

Hospital costs vary according to how much they must spend to provide patient care, as opposed to how much a patient or insurer must spend to receive care. The hospital earns a surplus when they receive higher amounts than their costs. They incur a loss when the opposite occurs.

Hospital costs vary according to how much they must spend to provide patient care, as opposed to how much a patient or insurer must spend to receive care. The hospital earns a surplus when they receive higher amounts than their costs. They incur a loss when the opposite occurs.

Cost–to-Charge Ratios & Their Relevance

As discussed earlier total charges do not reflect the payment received by the hospital and they do not reflect the actual cost to the hospital of providing patient care. Instead, hospitals typically compare their total charges to their cost using a cost-to-charge ratio determination.

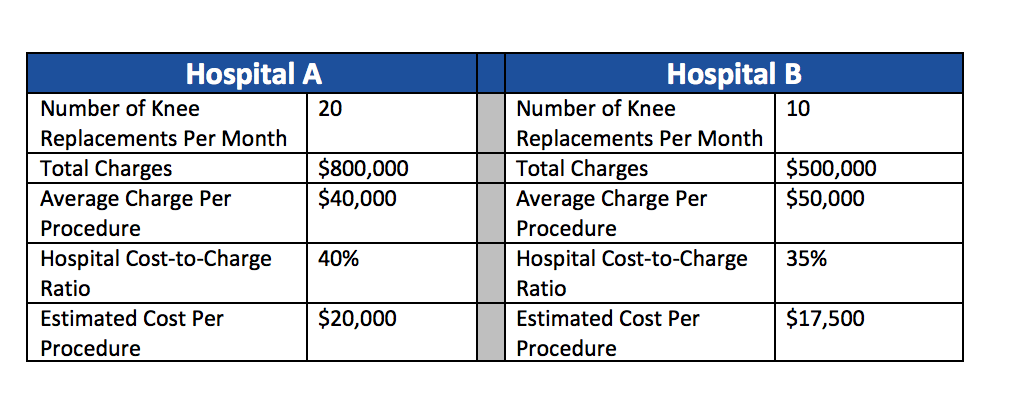

Here is how it works. The cost-to-charge ratio is the ratio between a hospital’s expenses and what they charge. The closer the cost-to-charge ratio is to 1, the less difference there is between the actual costs incurred and the hospital’s charges. Multiplying each hospital’s overall cost-to-charge ratio by total charges provides an estimate of the hospital’s costs.

The cost-to-charge ratio can be used to estimate the cost of some specific procedures or to compare hospital costs between different facilities in the same local area or in other areas of the country.

The example below compares the cost of two hospitals providing knee replacements. Both are located within the same city. Based on average charges per procedure, Hospital B appears more expensive for knee replacements. Hospital B’s lower cost-to-charge ratio, however, means that it performed each of the hip replacements at a lower average estimated cost than Hospital A.

If you were a consumer wouldn’t you be confused? This is exactly why price transparency is needed. Insurers need to know a fixed price it will cost them for a procedure and consumers need to know what their out-of-pocket costs will be for these and other common procedures.

Parting Thoughts

Price transparency initiatives are being pushed from the federal government, state governments, employers, consumers, and other stakeholders.![]() 1 Consumers, whether they be individuals, corporations or insurers want to understand the costs of inpatient and outpatient care in order to make better and more informed purchasing decisions. “The Center for Medicare and Medicaid Services (“CMS”) took steps in the fiscal year (“FY”) 2015 Inpatient Prospective Payment System (“IPPS”) final rule to implement the Affordable Care Act’s (“ACA”) provision requiring hospitals to establish and make public a list of its standard charges for items and services. In the final rule, CMS reminded hospitals of this requirement and reiterated that they encourage providers to move beyond just the required charge transparency and assist consumers in understanding their ultimate financial responsibility.”2

1 Consumers, whether they be individuals, corporations or insurers want to understand the costs of inpatient and outpatient care in order to make better and more informed purchasing decisions. “The Center for Medicare and Medicaid Services (“CMS”) took steps in the fiscal year (“FY”) 2015 Inpatient Prospective Payment System (“IPPS”) final rule to implement the Affordable Care Act’s (“ACA”) provision requiring hospitals to establish and make public a list of its standard charges for items and services. In the final rule, CMS reminded hospitals of this requirement and reiterated that they encourage providers to move beyond just the required charge transparency and assist consumers in understanding their ultimate financial responsibility.”2

- Smith Matthew: The Push for Hospital Price Transparency: How is Your Organization Responding? The Camden Group, June 2, 2015

- The National Conference of State Legislatures, 2015

As always we welcome your thoughts and input. Feel free to start a discussion.